Luxury Products: Running Up the Downward Escalator

CNN; The Wall Street Journal; Rolex

A Hermès Birkin handbag continues to appreciate on both retail and secondary markets. A new Rolex Submariner commands a multi-year wait at authorized dealers and routinely sells above MSRP on the pre-owned market. Ferrari caps annual production well below demand, with waitlists extending years into the future. From the outside, these products appear to defy commoditization: the slow erosion of perceived value as customer knowledge accumulates. Every market rides this downward escalator. But luxury appears to be an exception.

The Ofmos Theory of Business is a first-principles account of how products, companies, and economies behave. It is built from foundational observations about individual behavior rather than from empirical generalizations. It claims commoditization is structural: no offering is exempt, in any market, ever. The luxury cases look like a problem for the theory. They are not. Properly understood, they are the strongest evidence for it. The visible stillness (the unchanged product, the steady price, the consistent demand) is the surface effect of continuous, deliberate, exhausting work underneath. Stop the work for a year, and the stillness collapses. Pierre Cardin in the 1980s and Burberry in the early 2000s, among others, demonstrated this directly.

1. Commoditization — The Force That Always Wins

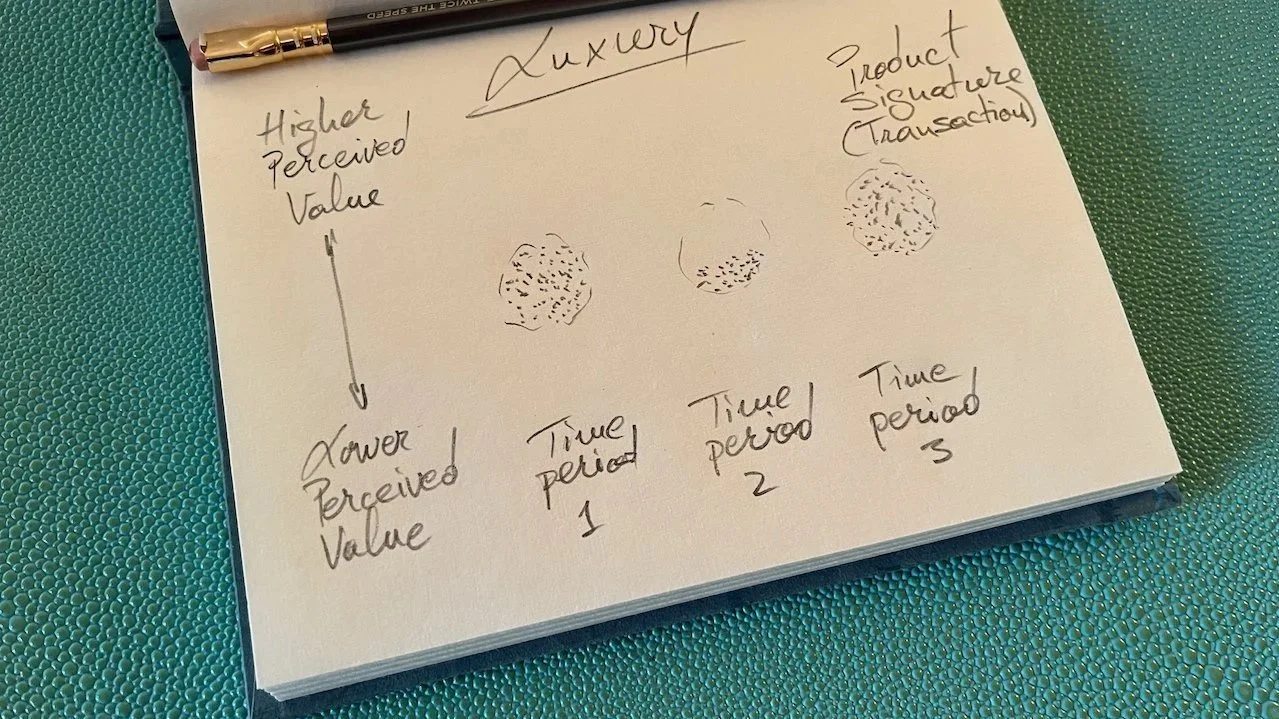

The customer who has owned three Birkins knows more about leather sourcing, stitching variation, waitlist mechanics, and resale dynamics than the customer who has owned none. The accumulated knowledge does not change the bag. But it changes what the customer engages with when they use it. As knowledge accumulates, new needs are created above the current one to enable the individual to make the most of their circumstances, pushing the original need lower in the hierarchy. What was once unfamiliar becomes routine. The vendor's offering has not changed, but what the customer engages with has. The Ofmos Theory calls what the customer engages with the experienced product, and its shrinking and drifting cluster of transactions is the observable signature of the change.

This is commoditization. It is not a property of the offering. It is a structural force that emerges when many customers participate in the same market over time, each learning, each generating new needs above the current one, each pushing the original need lower. The force erodes perceived value across the entire market, not just for one customer. It is always present, always directional, and for any specific offering in a stable environment, it always wins.

This understanding of value, grounded in the customer's experience rather than in the vendor's design, converges with service-dominant logic (Vargo & Lusch, 2004; Lusch & Vargo, 2014), which holds that value is determined by the customer in use, not by the producer in production. The Ofmos Theory reaches the same conclusion from a different starting point: the customer's hierarchical structure of needs.

In any market, the vendor has two choices. The first, and more natural, is to follow the customer's need as it drifts lower in the hierarchy. This typically means internal efficiencies that reduce price through higher volume, lower margins, or both. This is what most vendors do, and what commoditization looks like from the outside. The second is to work continuously to keep regenerating the experienced product at the higher-level boundary. This is what luxury strategists do.

2. Innovation — The Vendor's Response to Commoditization

The vendor's response to commoditization is innovation, deliberate strategic action that repositions the offering relative to the customer's perception. Looking at the product holistically and through the lens of transaction signature, the Ofmos Theory distinguishes between market innovation and product innovation. Market innovation repositions the offering toward higher perceived value by altering the external business conditions, without changing the offering. Product innovation is done by changing the offering itself: the scope of what it does and what it takes to produce. Most discussions of innovation focus on product innovation through engineering, the traditional form: deliberate design changes that add or remove features and capabilities of the offering itself. A smartphone with a better camera, a car with a more efficient engine, software with new functions. The vendor changes the offering, and the customer's experienced product shifts accordingly.

But engineering is not the only mechanism by which the experienced product is deliberately shifted. The theory identifies additional mechanisms that stem from design choices and go-to-market approaches rather than from changes to the offering's core functionality.

Product innovation through adoption occurs when the offering becomes more capable not because the vendor changed it, but because the network of users around it grew. A social network with one user is barely useful; with a million users, it becomes a way to maintain entire relationships. The product itself has not changed, but its capabilities have, because the network around it has activated capabilities that were latent. Network effects in the strict sense (Katz & Shapiro, 1985) sit here, but the literature has typically treated them as a market phenomenon rather than as a form of innovation. The Ofmos Theory treats them as a form of innovation, one that repositions the experienced product through a different mechanism than engineering.

Product innovation through discovery occurs when the customer gradually uncovers aspects of the offering that were present but not immediately apparent. An iPhone buyer who chose the device for calls and messaging discovers, over months of use, that holding the spacebar turns the keyboard into a trackpad, that the flashlight beam width is adjustable on certain models, that Back Tap triggers shortcuts, that a Shazam button is built into the control center. The customer's needs were never latent; they always wanted to do these things. What was latent was the customer's awareness that the offering already addressed them.

The offering does not change, but more of it enters the customer's experience as engagement with it deepens, thus expanding upward the cluster of transactions associated with it. This is rarely identified as innovation, but it is structurally the same kind of move: repositioning the experienced product without changing the offering itself. Most discussions of product innovation focus on engineering. Luxury strategy, as the following cases will show, depends on adoption and discovery to a degree that few other product categories do, with discovery doing the most distinctive work.

3. How Hermès Regenerates the Experienced Product

When Hermès manages scarcity through the allocation system, the purchase-history requirements, and the controlled releases, it is building a network of participants whose presence activates dimensions of the offering that would not exist for a solitary buyer. The experience of being allocated, of having earned access, of belonging to a group that money alone cannot enter, is part of the offering. But these capabilities are activated by the community around the product, not by engineering changes to the bag itself. A Birkin without the allocation ecosystem, without the collector community, without the secondary-market dynamics, is structurally a different product. This is the same mechanism as the social network example above, product innovation through adoption, achieved through go-to-market design rather than technology.

Hermès also deploys product innovation through discovery. The leather develops a patina through sustained use. The saddle stitch tightens over time. The single-artisan construction becomes visible to the owner through handling and wear. These are real functional properties that reveal themselves through engagement, not marketing narrative. The same discovery mechanism is at work here: the iPhone owner who uncovers a hidden capability and the Hermès owner who discovers the patina are undergoing the same process, though the discoverable dimensions are physical rather than digital.

When Hermès controls distribution through own boutiques, no outlet stores, and careful management of secondary-market narratives, it is preserving the conditions under which both mechanisms remain active. Sell the Birkin in a department store, and the adoption network collapses: there is no earned-access community left. The scarcity signal evaporates. The brand drops onto the same downward path as every other handbag.

Hermès also does market innovation, repositioning the offering toward higher perceived value by altering external business conditions to address higher-level needs. Pricing is the visible mechanism: the price signals that the bag belongs in a life defined by access most people cannot buy. But the bulk of the strategic work is adoption-side. The offering itself stays largely where it is.

4. Pierre Cardin, Burberry, and the Undefended Experienced Product

If luxury products genuinely defied commoditization, then a luxury brand that stopped innovating would maintain its position. The luxury industry behaves as if it knows this is false, and the historical record confirms the behavior.

Pierre Cardin built one of the most recognized names in twentieth-century fashion. Then he extended his name through licensing: by 1988, more than 800 licenses across 94 countries, on everything from baseball caps and cigarettes to toilet seat covers and frying pans. Each license destroyed the adoption network: the community of earned access dissolved as the brand became universally available. There was no scarcity-activated dimension left. Simultaneously, there was nothing left for the customer to discover. The offering had been made ordinary and ubiquitous. The experienced product did not shrink gradually. It was stripped to its basic capabilities overnight.

Burberry in the early 2000s showed a different version of the same dynamic. The signature check pattern, once a symbol of British luxury heritage, became widely associated with counterfeit goods and a working-class subculture the British press labeled "chav." The adoption-side dimensions (the community of distinction, the earned-access signal) lost their hold. The customer's need for exclusivity no longer engaged what the offering signaled. Angela Ahrendts and Christopher Bailey's turnaround was a systematic rebuilding of both mechanisms: buying back licenses restored the conditions for adoption by re-creating scarcity; suing counterfeiters, removing the nova check from all but a small fraction of products, centralizing design, and refocusing the brand on its trench-coat heritage restored the conditions for discovery. They did not change the fundamental product. They rebuilt the network and the depth that make the experienced product worth engaging with.

Both cases demonstrate the same point. The commoditization force is always present. The stillness is the surface effect of continuous work. Stop the work, and the surface effect dissolves.

5. Engineering, Adoption, and Discovery at Ferrari and Rolex

Ferrari runs engineering, adoption, and discovery simultaneously. Hybrid powertrains, aerodynamic advances, and new materials do the engineering work, changing the offering itself. The production cap, the controlled distribution, and the collector community do the adoption work: the network of owners whose scarcity-participation activates dimensions of exclusivity that would not exist if Ferrari sold to everyone who could pay. The motorsport heritage and the depth of the driving experience do the discovery work, revealing themselves through engagement in a way that deepens the offering for the committed driver.

Ferrari itself has already been through this. After Fiat acquired a majority stake, production was pushed to over 4,500 cars per year by the early 1990s. Cars sat unsold on dealer lots. The adoption network dissolved: there were no waitlists, no earned access, no scarcity-activated dimensions left. When Luca di Montezemolo returned as chairman in 1991, his turnaround was structurally the same move Angela Ahrendts made at Burberry: he cut production nearly in half, rebuilt the conditions for adoption by re-creating scarcity, and restored the conditions for discovery by deepening the ownership experience. He did not change the fundamental product. He rebuilt the network and the depth around it.

CEO Benedetto Vigna has explicitly stated the philosophy that emerged from that turnaround: production is intentionally kept "one car below market demand." Older models are phased out as new ones are introduced. Ferrari refuses to keep prior-generation cars in production for price-sensitive buyers, which would be the conventional move of following the need downward.

The Submariner has been refined incrementally since its 1953 introduction, but the design language is recognizably consistent across seven decades; the engineering mechanism is present but understated. The bulk of the innovation work happens through the adoption mechanism: the allocation system that signals earned access, the secondary-market premium that signals investment-grade value, the collector community whose participation activates the offering's exclusivity dimension. The offering itself stays largely where it is. The network around it regenerates the experienced product.

If Rolex expanded production to meet demand, the adoption network would dissolve. The allocation premium would vanish, the scarcity signal would evaporate, and the community-activated dimensions of the offering would have nothing left to engage the customer with. The experienced product would shrink to its basic capabilities, and Rolex would enter the same commoditization dynamic as every other watchmaker. The downward path was always there. Rolex's achievement is making it irrelevant by running upward fast enough on the adoption side that the offering itself never has to change.

6. The Perceived Stillness Is Innovation

The Ofmos Theory grounds strategy (the ongoing work of repositioning offerings against the commoditization force and the competitive pressure) in a structural claim about why continuous effort is necessary. The force is continuous. The strategist's response must be continuous. The two are inseparable.

Generally, the more common response is to follow the customer's need as it drifts lower, reducing price, increasing volume, accepting lower margins. The offering keeps generating revenue, but only because the vendor keeps surrendering position. Luxury providers refuse to surrender position. They work continuously to keep the offering at higher perceived value, altering business conditions, refining the offering, building the network around it, and preserving the conditions under which the customer keeps finding new depth in it.

Pierre Cardin destroyed his brand by flooding the market with reasons to learn it as ordinary. Burberry lost its position and rebuilt it by restoring the conditions for adoption and discovery. Hermès, Ferrari, and Rolex have never stopped running, and that is why their offerings appear, from the outside, to defy a force that acts on every offering in every market. They are not defying it. They are making it irrelevant by running harder than anyone is supposed to have to run. The effort, continuous, deliberate, never finished, is the strategy. The stillness is what the effort produces.

That is the race luxury pretends isn't happening.

References

Katz, M.L. & Shapiro, C. (1985). "Network Externalities, Competition, and Compatibility." American Economic Review, 75(3), 424–440.

Lusch, R.F. & Vargo, S.L. (2014). Service-Dominant Logic: Premises, Perspectives, Possibilities. Cambridge University Press.

Vargo, S.L. & Lusch, R.F. (2004). "Evolving to a New Dominant Logic for Marketing." Journal of Marketing, 68(1), 1–17.

—

The theoretical foundation of the argument, the One-Need Theory of Behavior and the Ofmos Theory of Business, is developed in detail at ofmos.com/the-foundational-theories.

—

Sources

Opening claims. Hermès Birkin: Sotheby's reports a long-term compound annual growth rate of approximately 5% on retail prices over forty years (sothebys.com, January 2026). Rebag's 2025 Clair Report, as reported by Robb Report, found that Birkins appreciated 92% on the preowned market over the last decade (robbreport.com, December 2025). Rolex Submariner: Multi-year wait lists at authorized dealers and secondary-market premiums of 30–70% above MSRP are documented in Bob's Watches' 2025 Submariner Market Report (bobswatches.com, January 2026). Ferrari: Ferrari N.V. shipped 13,752 units in 2024 with an order book extending into 2027 (Ferrari N.V. Q4 and Full Year 2024 results; Motor1, February 2025).

Pierre Cardin licensing. By 1986, Cardin had 800 licenses worldwide and 160,000 people employed under his brand (WWD, reported in Highsnobiety's "Digging Deeper" feature, November 2015). By 1988, the brand was on more than 800 licenses across 94 countries (Reddy and Terblanche 2005, cited in Tandfonline's "With License to Change," 2025). Product categories included toilet seat covers, cigarettes, sardines, frying pans, baseball caps, and pens. Cardin's own quote from a 2002 New York Times interview: "If someone asked me to do toilet paper, I'd do it. Why not?”

Burberry brand dilution, early 2000s. The check pattern's adoption by counterfeiters and association with "chav" culture is documented across multiple sources, including Wikipedia (en.wikipedia.org/wiki/Burberry), Grailed's "The History of Burberry's Check," and Fashionista's account of the brand's response (fashionista.com, February 2023).

Burberry turnaround. Angela Ahrendts (CEO from 2006) and Christopher Bailey (Creative Director from 2001) repurchased licensing agreements, sued counterfeiters, scaled back the check pattern from approximately 20% to 5% of products, centralized design, and refocused on the trench-coat heritage. By 2012, revenues had more than doubled to roughly $3 billion. Interbrand ranked Burberry the fourth fastest-growing brand in the world in 2011 (Second Acts Substack analysis, January 2025; Highsnobiety, February 2018; Wikipedia).

Ferrari production philosophy. CEO Benedetto Vigna's stated approach: "Ferrari will always deliver one car less than the market demand" (Ferrari 2022 Capital Markets Day). Ferrari's 2030 Strategic Plan reaffirms: "we will continue to preserve exclusivity staying true to our founder's belief to sell one car less than the market demands" (ferrari.com, October 2025). Ferrari believes wait lists should not exceed two years because longer waits upset buyers, particularly newer customers (Motor1, October 2025).

Ferrari turnaround under Montezemolo. Production reached 4,309 units in 1990 under Fiat management and was cut to 2,353 by 1993 after Luca di Montezemolo was appointed chairman in 1991 (Ferrari production data reported by Ferrari Lake Forest; Montezemolo biography, Wikipedia). Return to profitability by 1997 documented across multiple sources including the Acquired podcast's Ferrari episode (acquired.fm, April 2026), which includes a direct interview with Montezemolo.